Lawyer Tax Optimization: Legal Professional Strategies

Being a lawyer is tough. Long hours, demanding clients, and constantly evolving laws keep you on your toes. But amidst all the legal complexities, one area often gets overlooked: your own taxes. Are you paying more than you should? Are you leveraging all available deductions and credits? Let's dive into strategies designed to help legal professionals optimize their tax situation.

Many lawyers feel overwhelmed by the intricacies of the tax code. They might worry about making mistakes, missing deadlines, or simply not knowing what options are available to them. This can lead to stress, frustration, and ultimately, a financial burden that impacts their practice and personal life.

The goal of tax optimization for lawyers is to legally minimize your tax liability, freeing up more capital for reinvestment in your practice, personal investments, or simply enhancing your financial security. It’s about making informed decisions throughout the year, not just scrambling at tax time.

This article explores various tax optimization strategies specifically tailored for legal professionals. We'll delve into understanding business structures, claiming legitimate deductions, maximizing retirement contributions, and planning for long-term financial well-being. By implementing these strategies, lawyers can take control of their finances and build a more secure future. Keywords: tax optimization, lawyers, legal professionals, deductions, credits, retirement planning, business structure.

Understanding Business Structures for Tax Efficiency

Choosing the right business structure is paramount for tax optimization. I remember when I first started my practice, I defaulted to a sole proprietorship, thinking it was the simplest route. Big mistake! I soon realized I was missing out on significant tax advantages. After consulting with a tax advisor, I switched to an S-corp, which allowed me to pay myself a reasonable salary and then take the remaining profits as distributions, which are subject to self-employment taxes. This one change saved me thousands of dollars each year. The key is to understand the implications of each structure – sole proprietorship, partnership, LLC, S-corp, C-corp – and choose the one that aligns with your financial goals and risk tolerance. A sole proprietorship offers simplicity but limited liability protection. A partnership can be a good option for collaborating attorneys. LLCs provide liability protection and flexibility in taxation. S-corps and C-corps offer more complex structures with potential tax benefits for higher-earning lawyers. Carefully weigh the pros and cons with a qualified professional to determine the best fit for your specific circumstances. Consider factors like your income level, risk tolerance, and long-term business plans. Ignoring this crucial step can leave substantial money on the table come tax season. The right structure can significantly impact your tax burden and your firm's overall financial health. Keywords: business structure, sole proprietorship, partnership, LLC, S-corp, C-corp, tax efficiency, liability protection.

Maximizing Deductions for Legal Professionals

Deductions are your best friend when it comes to lowering your taxable income. Many lawyers fail to fully utilize all available deductions because they are unaware of them or lack proper record-keeping. Common deductions for lawyers include expenses related to continuing legal education (CLE), professional organization memberships, subscriptions to legal journals, and home office expenses if you have a dedicated workspace in your home. Don't overlook deductions for client development activities, such as meals and entertainment, subject to certain limitations. Also, carefully track your travel expenses for business purposes, including transportation, lodging, and meals. Remember to keep detailed records and receipts to substantiate your deductions in case of an audit. Utilizing tax software or working with a tax professional can help you identify and claim all eligible deductions. Proactive planning and meticulous record-keeping are essential to maximizing your tax savings. Furthermore, be aware of any changes in tax laws that may impact the deductions you can claim. Staying informed and seeking expert advice will ensure you're not leaving any money on the table. Keywords: deductions, legal professionals, CLE, professional memberships, home office, client development, travel expenses, record-keeping.

Strategic Retirement Planning for Lawyers

Retirement planning is not just about saving for the future; it's also a powerful tool for tax optimization. Lawyers have several options for retirement savings, including 401(k)s, solo 401(k)s, SEP IRAs, and defined benefit plans. Contributing to these plans can provide significant tax advantages, such as reducing your taxable income and allowing your investments to grow tax-deferred or even tax-free (in the case of Roth accounts). The best option for you will depend on your income level, business structure, and retirement goals. A solo 401(k) can be particularly attractive for self-employed lawyers, as it allows you to contribute both as an employer and an employee, significantly increasing your potential savings. SEP IRAs are simpler to set up but may have lower contribution limits. Defined benefit plans can be more complex but offer the potential for higher contributions and tax deductions. Consult with a financial advisor to determine the most suitable retirement plan for your individual circumstances. Regular contributions to a tax-advantaged retirement account not only secure your financial future but also provide immediate tax relief. Don't wait until retirement is around the corner to start planning; the sooner you start, the greater the potential tax savings and the more comfortable your retirement will be. Keywords: retirement planning, 401(k), solo 401(k), SEP IRA, defined benefit plan, tax advantages, financial advisor.

The Myth of "Too Much Income" for Tax Planning

A common misconception is that tax planning is only beneficial for those with lower incomes. In reality, high-income earners, including successful lawyers, often have the most to gain from strategic tax planning. With higher income comes a higher tax bracket, which means that even small deductions and credits can result in substantial tax savings. Furthermore, high-income earners may be subject to additional taxes, such as the alternative minimum tax (AMT) or the net investment income tax. Effective tax planning can help mitigate the impact of these taxes and ensure that you're not paying more than you legally owe. Strategies such as maximizing retirement contributions, utilizing tax-loss harvesting, and investing in tax-advantaged investments can be particularly beneficial for high-income lawyers. Don't assume that your income level makes tax planning irrelevant; on the contrary, it makes it even more critical. Seek professional guidance to develop a customized tax plan that addresses your specific financial situation and maximizes your tax savings potential. Ignoring tax planning simply because you earn a high income can be a costly mistake. Keywords: high-income earners, tax planning, alternative minimum tax (AMT), net investment income tax, tax-loss harvesting, tax-advantaged investments.

Tax-Loss Harvesting Explained

Tax-loss harvesting is a strategy that involves selling investments that have decreased in value to offset capital gains. This can be a particularly useful technique for lawyers who have a diverse investment portfolio. By realizing losses on underperforming investments, you can reduce your overall tax liability on capital gains. The losses can be used to offset gains in the current year, and any remaining losses can be carried forward to future years. However, it's important to be aware of the "wash sale" rule, which prevents you from repurchasing a substantially identical investment within 30 days of selling it at a loss. This rule is designed to prevent taxpayers from artificially generating losses for tax purposes. To effectively implement tax-loss harvesting, it's crucial to monitor your investment portfolio regularly and identify opportunities to realize losses. Work closely with a financial advisor to develop a strategy that aligns with your investment goals and risk tolerance. Tax-loss harvesting can be a valuable tool for reducing your tax burden and improving your overall investment returns, but it requires careful planning and execution. Don't attempt to implement this strategy without a thorough understanding of the rules and regulations involved. Keywords: tax-loss harvesting, capital gains, wash sale rule, investment portfolio, financial advisor.

Tax Planning Tips Throughout the Year

Tax planning should not be a once-a-year activity; it should be an ongoing process throughout the year. By proactively managing your finances and making informed decisions throughout the year, you can significantly improve your tax outcome. Some key tips for year-round tax planning include: tracking your income and expenses regularly, reviewing your estimated tax payments, adjusting your W-4 form if necessary, and documenting all deductible expenses. Consider setting up a separate bank account and credit card for business expenses to make tracking easier. Review your tax situation with a qualified professional at least once a year to identify potential opportunities and address any concerns. Don't wait until the last minute to gather your documents and prepare your tax return; start early to avoid errors and ensure you're not missing any deductions or credits. Stay informed about changes in tax laws and regulations that may impact your tax situation. Proactive tax planning can help you minimize your tax liability, avoid penalties, and achieve your financial goals. It's an investment in your financial well-being that will pay dividends for years to come. Keywords: tax planning, year-round tax planning, estimated tax payments, W-4 form, deductible expenses, tax professional.

The Importance of Professional Guidance

While this article provides general information about tax optimization strategies for lawyers, it's not a substitute for professional advice. Every lawyer's financial situation is unique, and the best tax plan will depend on your individual circumstances. A qualified tax advisor or accountant can help you assess your financial situation, identify potential tax savings opportunities, and develop a customized tax plan that aligns with your goals. They can also help you navigate the complexities of the tax code and ensure that you're in compliance with all applicable laws and regulations. Don't hesitate to seek professional guidance, especially if you have a complex financial situation or are unsure about any aspect of tax planning. The cost of professional advice is often outweighed by the tax savings and peace of mind it provides. Consider it an investment in your financial future. Furthermore, a good tax advisor can provide ongoing support and guidance throughout the year, helping you stay on track and make informed financial decisions. Keywords: tax advisor, accountant, professional guidance, customized tax plan, financial situation, tax savings.

Fun Facts About Tax Law

Tax law can be surprisingly fascinating, with a rich history and quirky provisions. Did you know that the U.S. tax code is one of the longest and most complex in the world? Or that the first income tax in the United States was introduced during the Civil War to finance the war effort? Throughout history, tax laws have been used to fund wars, promote social policies, and influence economic behavior. Some tax laws are downright bizarre, such as taxes on specific items or activities that seem arbitrary or outdated. Exploring the history and evolution of tax law can provide a deeper understanding of its impact on society and the economy. While tax law can be complex and challenging, it's also a reflection of our values and priorities as a nation. Understanding the history and context behind tax laws can make the process of tax planning more engaging and less daunting. So, next time you're struggling with your taxes, take a moment to appreciate the long and winding road that tax law has taken to get to where it is today. Keywords: tax law, history of tax law, U.S. tax code, income tax, tax policy.

How to Find a Good Tax Advisor

Finding the right tax advisor is crucial for successful tax optimization. Start by seeking referrals from colleagues, friends, or other professionals in your network. Look for a tax advisor who has experience working with lawyers or other legal professionals. Check their credentials and qualifications to ensure they are licensed and in good standing. Ask about their fees and how they charge for their services. It's important to find someone who is knowledgeable, responsive, and trustworthy. Schedule a consultation to discuss your financial situation and assess their understanding of your needs. Don't be afraid to ask questions and get a clear understanding of their approach to tax planning. A good tax advisor will be proactive, communicate clearly, and provide valuable insights and recommendations. Trust your gut feeling; if you don't feel comfortable with a particular advisor, move on to someone else. The relationship with your tax advisor is a long-term partnership, so it's important to find someone you can trust and work with effectively. Keywords: tax advisor, finding a tax advisor, referrals, credentials, fees, consultation.

What If I Get Audited?

The prospect of a tax audit can be daunting, but it's important to remain calm and prepared. If you receive a notice of audit, the first step is to contact your tax advisor or accountant. They can help you understand the audit process, gather the necessary documentation, and represent you before the IRS. Don't ignore the audit notice or try to handle it on your own; professional assistance is essential. Cooperate fully with the IRS and provide all requested information in a timely manner. Keep detailed records of all income and expenses, as well as any supporting documentation. An audit doesn't necessarily mean you've done anything wrong; it simply means the IRS wants to verify the accuracy of your tax return. With proper preparation and professional guidance, you can navigate the audit process with confidence and minimize any potential negative consequences. Remember, honesty and transparency are key when dealing with the IRS. Keywords: tax audit, IRS audit, audit process, tax advisor, record-keeping.

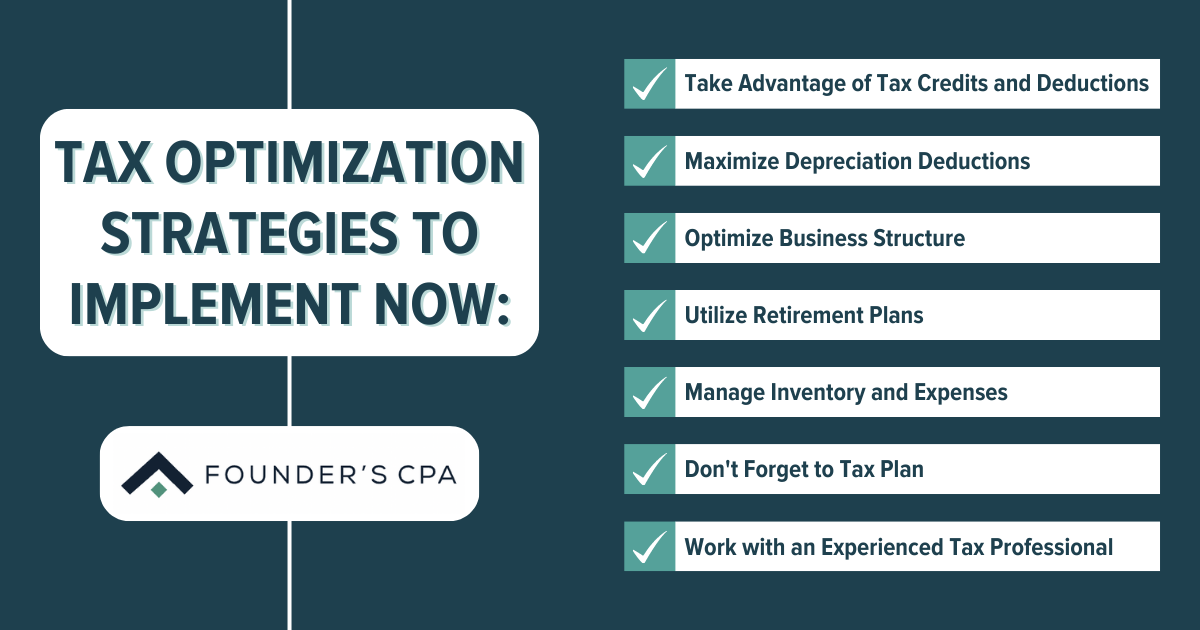

Tax Optimization Checklist for Lawyers: A Listicle

Here's a quick checklist to help you get started with tax optimization: 1. Choose the right business structure.

2. Maximize your deductions.

3. Strategically plan for retirement.

4. Track your income and expenses diligently.

5. Review your estimated tax payments regularly.

6. Document all deductible expenses.

7. Seek professional guidance from a qualified tax advisor.

8. Stay informed about changes in tax laws.

9. Plan for long-term financial well-being.

10. Don't be afraid to ask questions. By following these simple steps, you can take control of your taxes and build a more secure financial future for yourself and your practice. Tax optimization is not a one-time fix; it's an ongoing process that requires attention and effort. But the rewards are well worth it. The knowledge and guidance of a professional can transform your tax situation to ensure you are claiming all eligible expenses and avoiding problems with the IRS. Keywords: tax optimization checklist, business structure, deductions, retirement planning, income and expenses, tax advisor.

Question and Answer

Q: What is the biggest tax mistake lawyers make?

A: Failing to track all deductible expenses and not choosing the most advantageous business structure are common mistakes.

Q: How often should I review my tax plan?

A: At least once a year, but ideally more frequently, especially if your income or business structure changes.

Q: Can I deduct my home office expenses?

A: Yes, if you use a portion of your home exclusively and regularly for business purposes.

Q: What are the benefits of working with a tax advisor?

A: A tax advisor can help you identify tax savings opportunities, navigate the complexities of the tax code, and ensure you're in compliance with all applicable laws.

Conclusion of Lawyer Tax Optimization: Legal Professional Strategies

Optimizing your tax situation as a lawyer requires a proactive and strategic approach. By understanding your options, seeking professional guidance, and implementing effective tax planning strategies, you can minimize your tax liability and maximize your financial well-being. Don't let taxes be an afterthought; make them a priority, and you'll reap the rewards for years to come. Remember to regularly review your tax plan, stay informed about changes in tax laws, and seek professional guidance when needed. Take control of your finances and build a more secure future.

Post a Comment