Roth IRA Conversion: Tax-Smart Retirement Planning

Imagine a future where your retirement savings grow tax-free, and you don't have to worry about paying taxes when you withdraw them. Sounds like a dream, right? Well, it's not just a dream; it's a possibility with a Roth IRA conversion. But understanding the nuances of this strategy is key to unlocking its full potential.

Many people feel overwhelmed by the complexities of retirement planning. The constant changes in tax laws, coupled with the fear of making the wrong financial decisions, can leave individuals feeling stuck and unsure of how to proceed. The thought of navigating complicated tax rules and potential penalties can be paralyzing.

This article aims to demystify the Roth IRA conversion process, providing you with the knowledge and confidence to make informed decisions about your financial future. We'll break down the intricacies of Roth IRA conversions, explore the benefits and drawbacks, and help you determine if this strategy is right for you. Our goal is to empower you to take control of your retirement savings and minimize your tax burden.

In summary, we've explored the core aspects of Roth IRA conversions, including their purpose, mechanics, and potential benefits. We've also delved into common misconceptions, hidden secrets, and strategic considerations to help you make informed decisions. Key terms like Roth IRA, traditional IRA, tax-free growth, tax bracket, and backdoor Roth IRA have been explained in detail. Now, let's get into the details of Roth IRA Conversion: Tax-Smart Retirement Planning.

Understanding the Roth IRA Advantage

The target of understanding the Roth IRA Advantage is to emphasize the benefits of Roth IRAs, such as tax-free growth and withdrawals in retirement, and how this advantage can be amplified through strategic conversions.

I remember when I first started learning about retirement planning, the Roth IRA concept felt like magic. The idea of never paying taxes on my investment gains in retirement seemed too good to be true. But as I dug deeper, I realized that the Roth IRA's tax advantages are a powerful tool for long-term wealth accumulation.

The beauty of a Roth IRA lies in its tax treatment. Unlike a traditional IRA, where contributions are tax-deductible but withdrawals are taxed in retirement, a Roth IRA works in reverse. You contribute after-tax dollars, but your investments grow tax-free, and withdrawals in retirement are also tax-free. This can be a significant advantage, especially if you anticipate being in a higher tax bracket in retirement.

A Roth IRA conversion allows you to move funds from a traditional IRA (which is funded with pre-tax dollars) to a Roth IRA. While you'll pay taxes on the converted amount in the year of the conversion, all future growth and withdrawals from the Roth IRA will be tax-free. The key is to convert when your tax bracket is relatively low, maximizing the long-term benefits.

Think of it as planting a tree today so you can enjoy its shade for years to come. While you might have to put in some effort to plant the tree (paying taxes on the converted amount), the long-term rewards (tax-free growth and withdrawals) can be well worth it.

What is a Roth IRA Conversion?

The target of explaining "What is a Roth IRA Conversion?" is to provide a clear and concise definition of Roth IRA conversions, including the process, tax implications, and eligibility requirements.

A Roth IRA conversion is essentially the act of transferring funds from a traditional IRA (or other pre-tax retirement account) into a Roth IRA. The key distinction is that the money in a traditional IRA hasn't been taxed yet, while Roth IRA contributions are made with after-tax dollars. So, when you convert, you're essentially paying income tax on the amount you're converting.

Let's break it down further. Imagine you have $50,000 in a traditional IRA. If you decide to convert it to a Roth IRA, that $50,000 will be treated as taxable income in the year you make the conversion. You'll need to include it on your tax return and pay taxes at your current income tax rate.

Once the funds are in the Roth IRA, however, they grow tax-free, and qualified withdrawals in retirement are also tax-free. This is where the long-term advantage comes in. If you believe your tax rate will be higher in retirement, a Roth IRA conversion can be a smart move. You're paying taxes now at a lower rate to avoid potentially higher taxes later.

Eligibility for a Roth IRA conversion is generally straightforward. There are no income limitations on who can convert to a Roth IRA. However, it's crucial to consider your current tax situation and future retirement plans before making the conversion. It's also important to remember that once you convert, the conversion is generally irreversible.

History and Myths of Roth IRA Conversion

The goal of discussing the "History and Myths of Roth IRA Conversion" is to dispel common misconceptions and provide a historical context for the Roth IRA conversion strategy, highlighting its evolution and addressing prevalent myths.

The Roth IRA, named after former Senator William Roth, was created as part of the Taxpayer Relief Act of 1997. It offered a new way to save for retirement, with tax-free growth and withdrawals as the main selling point. Initially, Roth IRA conversions were more restrictive, but over time, the rules have evolved, making them more accessible to a wider range of individuals.

One of the biggest myths surrounding Roth IRA conversions is that they're only beneficial for the wealthy. While high-income earners can certainly benefit, Roth conversions can be a valuable tool for anyone who anticipates being in a higher tax bracket in retirement or who simply wants the peace of mind of tax-free withdrawals.

Another common myth is that you should never convert to a Roth IRA if the market is down. While it's true that you'll be paying taxes on the converted amount, converting during a market downturn can actually be advantageous. Because your investments have decreased in value, the tax burden of the conversion will be lower. And when the market recovers, all that growth will be tax-free.

It's also a myth that Roth IRA conversions are too complicated to understand. While there are certainly nuances to consider, the basic concept is relatively simple: you pay taxes now to avoid taxes later. With careful planning and professional guidance, Roth IRA conversions can be a powerful tool for tax-smart retirement planning.

Hidden Secrets of Roth IRA Conversion

The target of revealing the "Hidden Secrets of Roth IRA Conversion" is to uncover lesser-known strategies and considerations related to Roth IRA conversions, such as recharacterization rules (if applicable), tax planning opportunities, and strategies for minimizing the tax impact.

One of the "hidden secrets" of Roth IRA conversions lies in the potential for tax planning. By strategically converting smaller amounts over several years, you can potentially stay within a lower tax bracket and minimize the tax impact of the conversion. This is particularly useful if you're close to the edge of a tax bracket.

Another secret is the potential to use Roth IRA conversions as a tool for estate planning. Because Roth IRAs are not subject to required minimum distributions (RMDs) during the original owner's lifetime, they can be a valuable asset to pass on to heirs. And since Roth IRA withdrawals are tax-free for beneficiaries, this can provide significant tax savings for future generations.

For those who are charitably inclined, a qualified charitable distribution (QCD) from a traditional IRA can be used to offset the tax liability of a Roth IRA conversion. This strategy involves donating directly from your IRA to a qualified charity, which can reduce your taxable income and make a Roth IRA conversion more tax-efficient.

Also, don't forget about the "backdoor Roth IRA," a strategy for high-income earners who are ineligible to contribute directly to a Roth IRA. By making nondeductible contributions to a traditional IRA and then converting those funds to a Roth IRA, you can effectively bypass the income limitations.

Recommendations for Roth IRA Conversion

The aim of "Recommendations for Roth IRA Conversion" is to provide actionable advice and recommendations based on individual circumstances, such as age, income, and retirement goals, to help readers determine if a Roth IRA conversion is a suitable strategy for them.

Before recommending a Roth IRA conversion, it's crucial to assess your individual circumstances. Consider your age, income, tax bracket, retirement goals, and risk tolerance. A Roth IRA conversion may be particularly beneficial if you are:

Younger and expect to be in a higher tax bracket in retirement.

In a low tax bracket currently and have the funds to pay the taxes on the conversion.

Looking for tax diversification in your retirement portfolio.

Concerned about potential future tax increases.

On the other hand, a Roth IRA conversion may not be the best strategy if you:

Are already in a high tax bracket.

Need the funds in your traditional IRA for immediate expenses.

Expect to be in a lower tax bracket in retirement.

It's also important to consult with a qualified financial advisor and tax professional to determine if a Roth IRA conversion is right for you. They can help you analyze your specific situation and develop a personalized plan that aligns with your financial goals. Remember, Roth IRA conversion is not a one-size-fits-all solution, and it's essential to weigh the pros and cons carefully before making a decision.

Tax Implications of Roth IRA Conversion

The goal of detailing "Tax Implications of Roth IRA Conversion" is to thoroughly explain the tax consequences of converting a traditional IRA to a Roth IRA, including how the converted amount is taxed and potential strategies for minimizing the tax impact.

The primary tax implication of a Roth IRA conversion is that the converted amount is treated as taxable income in the year of the conversion. This means that you'll need to include the converted amount on your tax return and pay taxes at your current income tax rate.

The tax implications of a Roth IRA conversion can be significant, especially if you're converting a large sum of money. It's essential to plan carefully and consider the potential tax consequences before making the conversion.

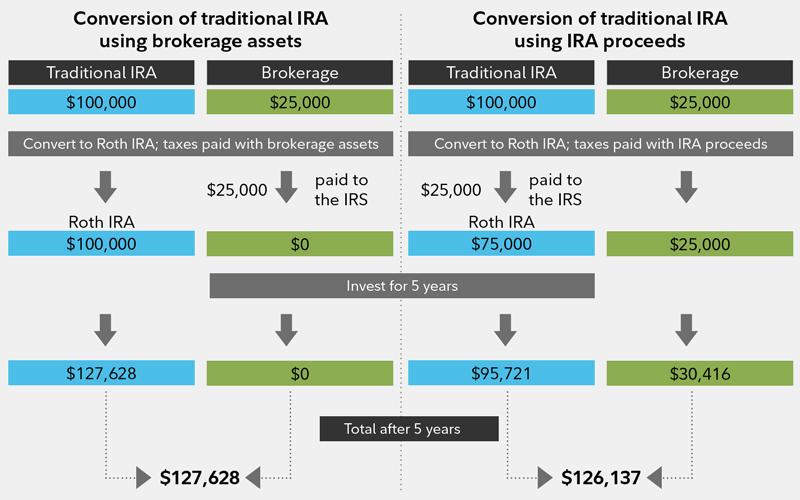

One strategy for minimizing the tax impact of a Roth IRA conversion is to convert smaller amounts over several years. This can help you stay within a lower tax bracket and avoid a large tax bill in a single year. Another strategy is to use deductions and credits to offset the taxable income from the conversion.

It's also important to remember that state taxes may apply to Roth IRA conversions. Some states may not offer the same tax advantages as the federal government, so it's essential to consult with a tax professional to understand the state tax implications of a Roth IRA conversion.

Tips for Successful Roth IRA Conversion

The target of "Tips for Successful Roth IRA Conversion" is to provide practical tips and strategies to ensure a smooth and effective Roth IRA conversion process, from planning and preparation to execution and ongoing management.

Planning is paramount for a successful Roth IRA conversion. Before you convert, take a close look at your finances. Project your income for the year. Estimate your tax bracket. Determine if you can comfortably pay the taxes due on the converted amount without jeopardizing your financial stability.

Consider converting during a year when your income is lower than usual. Perhaps you experienced a job loss, took time off work, or had significant deductible expenses. These circumstances can create a window of opportunity for a tax-efficient Roth conversion.

If you have multiple traditional IRA accounts, consider consolidating them before converting. This can simplify the conversion process and make it easier to track your assets. Also, keep meticulous records of your Roth IRA conversions. Document the amount converted, the date of the conversion, and any taxes paid. This information will be invaluable when you file your taxes and for future retirement planning.

Finally, remember that Roth IRA conversions are generally irreversible. Once you convert, you cannot change your mind. Therefore, it's crucial to carefully consider all the factors before making a decision.

Understanding the 5-Year Rule

The objective of “Understanding the 5-Year Rule” is to explain the 5-year rule associated with Roth IRA conversions and withdrawals, clarifying its implications for accessing converted funds and ensuring compliance with IRS regulations.

The 5-year rule for Roth IRAs can be tricky, but it's important to understand. There are actually two 5-year rules that apply to Roth IRAs: one for conversions and one for contributions.

The 5-year rule for conversions states that you must wait at least five years from the beginning of the tax year in which you made your first Roth IRA conversion before you can withdraw the converted funds tax-free and penalty-free. This rule applies separately to each conversion.

So, if you convert $10,000 from a traditional IRA to a Roth IRA in 2024, the 5-year clock starts on January 1, 2024. You won't be able to withdraw that $10,000 tax-free and penalty-free until January 1,

2029.

The 5-year rule for contributions states that you must wait at least five years from the date of your first Roth IRA contribution before you can withdraw any earnings tax-free and penalty-free. This rule only applies to the earnings portion of your Roth IRA. You can always withdraw your contributions tax-free and penalty-free, regardless of how long you've had the account.

Exceptions to the 5-year rule exist, such as for death, disability, or qualified first-time homebuyer expenses. However, it's essential to consult with a tax professional to determine if you qualify for an exception.

Fun Facts of Roth IRA Conversion

The aim of highlighting "Fun Facts of Roth IRA Conversion" is to share interesting and little-known facts about Roth IRA conversions to make the topic more engaging and memorable.

Did you know that the Roth IRA is named after the late Senator William Roth of Delaware? Senator Roth was a champion of tax reform and believed in empowering individuals to save for retirement.

Here's another fun fact: Roth IRAs are not subject to required minimum distributions (RMDs) during the original owner's lifetime. This means you can leave your money in the account to grow tax-free for as long as you live.

Interestingly, the IRS doesn't allow you to "undo" a Roth IRA conversion, except in very limited circumstances. Once you convert, it's generally a permanent decision. That's why it's so important to carefully consider all the factors before making a conversion.

And lastly, while you can't contribute more than the annual Roth IRA contribution limit, there's no limit on how much you can convert from a traditional IRA to a Roth IRA. This opens up significant opportunities for tax planning and wealth accumulation.

How to Start a Roth IRA Conversion?

The goal of explaining "How to Start a Roth IRA Conversion?" is to provide step-by-step instructions on initiating and completing a Roth IRA conversion, including opening a Roth IRA account, transferring funds, and reporting the conversion to the IRS.

The first step in starting a Roth IRA conversion is to open a Roth IRA account. If you don't already have one, you can open an account at a brokerage firm, bank, or other financial institution.

Once you have a Roth IRA account, you can initiate the conversion process. This typically involves contacting your traditional IRA custodian and requesting a direct transfer or a rollover of funds to your Roth IRA. A direct transfer is generally the preferred method, as it avoids the risk of missing the 60-day rollover deadline.

When you request the transfer, be sure to specify the exact amount you want to convert. You'll also need to provide your Roth IRA account information to the traditional IRA custodian.

After the funds are transferred, you'll need to report the conversion to the IRS. This is done by filing Form 8606, Nondeductible IRAs, with your tax return for the year in which you made the conversion.

It's essential to keep accurate records of your Roth IRA conversion. Document the amount converted, the date of the conversion, and any taxes paid. This information will be invaluable when you file your taxes and for future retirement planning.

Finally, consult with a tax professional to ensure that you're following all the necessary steps and that you're maximizing the tax benefits of your Roth IRA conversion.

What if Roth IRA Conversion?

The aim of exploring "What if Roth IRA Conversion?" is to address potential scenarios and outcomes associated with Roth IRA conversions, such as market fluctuations, tax law changes, and unexpected financial needs, and how to adjust your strategy accordingly.

What if the market crashes after you convert to a Roth IRA? This is a common concern, but it's important to remember that you're investing for the long term. Market fluctuations are inevitable, and a Roth IRA conversion is a long-term strategy that can still be beneficial even if the market experiences short-term declines.

What if tax laws change in the future? While it's impossible to predict the future, it's possible that tax rates will increase in the coming years. If this happens, a Roth IRA conversion could become even more valuable, as it would allow you to avoid paying higher taxes in retirement.

What if you need to access the converted funds before age 59 ½? As mentioned earlier, there are penalties for withdrawing converted funds before age 59 ½, unless you meet certain exceptions. However, you can always withdraw your contributions tax-free and penalty-free, regardless of your age.

What if you regret converting to a Roth IRA? Roth IRA conversions are generally irreversible, so it's important to carefully consider all the factors before making a decision. However, if you realize that a Roth IRA conversion was not the right choice for you, you may be able to mitigate the damage by adjusting your investment strategy or seeking professional financial advice.

Listicle of Roth IRA Conversion

The goal of providing a "Listicle of Roth IRA Conversion" is to present the key takeaways and benefits of Roth IRA conversions in a concise and easily digestible format, making the information more accessible and memorable.

- Tax-Free Growth: Your investments in a Roth IRA grow tax-free, allowing your savings to compound more quickly.

- Tax-Free Withdrawals: Qualified withdrawals in retirement are tax-free, providing predictable income.

- No Required Minimum Distributions (RMDs): You're not required to take distributions during your lifetime.

- Estate Planning Benefits: Roth IRAs can be passed on to heirs with potential tax advantages.

- Flexibility: You can withdraw contributions tax-free and penalty-free at any time.

- Potential for Higher Returns: By avoiding taxes on investment gains, you can potentially achieve higher returns over the long term.

- Protection Against Future Tax Increases: If tax rates rise in the future, your Roth IRA savings will be shielded from higher taxes.

- Tax Diversification: Roth IRAs provide tax diversification in your retirement portfolio.

- Opportunity for Roth IRA Conversions: You can convert traditional IRA funds to a Roth IRA, paying taxes now to avoid taxes later.

- Peace of Mind: Knowing that your retirement savings are growing tax-free can provide peace of mind and financial security.

Question and Answer about Roth IRA Conversion

Q: Who should consider a Roth IRA conversion?

A: Individuals who expect to be in a higher tax bracket in retirement, those seeking tax diversification, and those who want to leave a tax-advantaged inheritance to their heirs should consider a Roth IRA conversion.

Q: What are the potential drawbacks of a Roth IRA conversion?

A: The primary drawback is the immediate tax liability on the converted amount. Additionally, conversions are generally irreversible, and there may be penalties for withdrawing converted funds before age 59 ½, unless certain exceptions apply.

Q: How do I determine if a Roth IRA conversion is right for me?

A: Consult with a qualified financial advisor and tax professional. They can help you analyze your specific situation, assess your current and future tax brackets, and develop a personalized plan that aligns with your financial goals.

Q: Can I convert only a portion of my traditional IRA to a Roth IRA?

A: Yes, you can convert any amount you choose, from a small portion to the entire balance. Converting smaller amounts over several years can help minimize the tax impact of the conversion.

Conclusion of Roth IRA Conversion: Tax-Smart Retirement Planning

Roth IRA conversions offer a compelling strategy for tax-smart retirement planning. By understanding the intricacies of the conversion process, considering your individual circumstances, and seeking professional guidance, you can make informed decisions that align with your financial goals. While Roth IRA conversion might not be for everyone, the benefits of tax-free growth and withdrawals can be significant. Embrace the opportunity to take control of your retirement savings and potentially minimize your tax burden with a Roth IRA conversion.

Post a Comment