Bond Investment Tax Planning: Fixed Income Strategies

Imagine watching your investment portfolio grow steadily, providing a comfortable income stream. But what if a significant portion of those gains disappears when tax season rolls around? Navigating the complexities of bond investments and their tax implications can feel like traversing a minefield, but it doesn't have to be that way.

Many investors find themselves frustrated by the lack of clear, concise information on how taxes affect their bond portfolios. They struggle to understand the different types of bonds, their unique tax treatments, and the strategies available to minimize their tax liabilities. This confusion often leads to missed opportunities for tax-efficient investing, potentially diminishing their overall returns.

This article aims to shed light on the essential aspects of bond investment tax planning. We will explore various fixed income strategies and how to strategically manage your bond portfolio to reduce your tax burden while maximizing your investment returns.

By understanding the tax implications of different bond types (municipal, corporate, treasury), utilizing strategies like tax-loss harvesting and strategic asset allocation, and making informed decisions about account types (tax-advantaged vs. taxable), you can significantly enhance the after-tax performance of your bond investments. We'll delve into practical tips and considerations for building a tax-efficient fixed income portfolio.

Understanding Bond Taxation Basics

From my own experience, I recall inheriting a small bond portfolio from my grandmother. Naively, I assumed all bond income was treated the same for tax purposes. Boy, was I wrong! The first tax season after receiving the inheritance, I was shocked to discover the different tax rates applied to various bond types. Some were subject to federal income tax, while others, like municipal bonds, offered federal tax exemptions. It was a wake-up call that highlighted the importance of understanding the nuances of bond taxation.

Bonds, as fixed income investments, generate taxable income in several forms: coupon payments (periodic interest) and capital gains (profit from selling the bond for more than you paid). However, the tax treatment varies depending on the type of bond. U.S. Treasury bonds are subject to federal income tax but are exempt from state and local taxes. Corporate bonds are generally subject to both federal and state taxes. Municipal bonds, issued by state and local governments, offer a unique advantage: the interest income is typically exempt from federal income tax, and may even be exempt from state and local taxes if you reside in the state of issuance. This "triple tax-exemption" makes municipal bonds attractive to investors in high tax brackets.

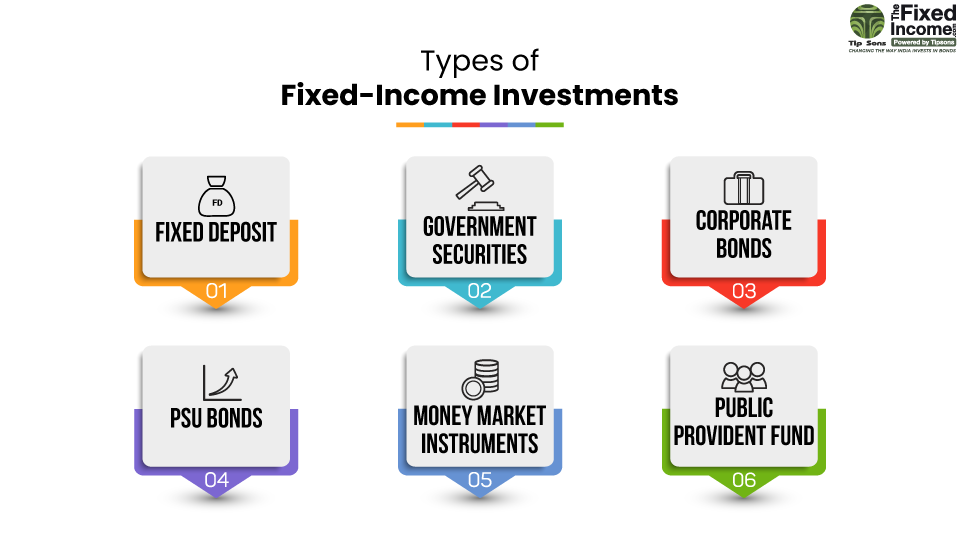

Types of Bonds and Their Tax Implications

What exactly are the different types of bonds and how do their tax implications differ? Let's break it down. Treasury bonds, backed by the full faith and credit of the U.S. government, are considered very safe investments. As mentioned, their interest income is taxable at the federal level but exempt from state and local taxes. This can be a significant benefit for investors living in states with high income taxes. Corporate bonds, issued by companies to raise capital, typically offer higher yields than Treasury bonds, but they also carry a higher risk of default. The interest income from corporate bonds is fully taxable at both the federal and state levels.

Municipal bonds, or munis, are debt obligations issued by state and local governments to finance public projects like schools, roads, and hospitals. The key attraction of munis is their tax-exempt status. Interest earned on most munis is exempt from federal income tax. Furthermore, if you purchase munis issued by your state of residence, the interest may also be exempt from state and local taxes, providing a "double" or even "triple" tax benefit. This makes munis particularly appealing to high-income earners in high-tax states. Understanding these differences is crucial for effective bond investment tax planning.

The History and Myths of Bond Investing

Throughout history, bonds have been perceived as safe and reliable investments, particularly during times of economic uncertainty. One common myth is that all bonds are equally safe. This is simply not true. The creditworthiness of the issuer plays a crucial role. Government bonds are generally considered the safest, while corporate bonds carry varying levels of risk depending on the financial health of the issuing company. Another myth is that bonds are always a low-yield investment. While bonds typically offer lower returns than stocks, they can provide a stable income stream and diversify a portfolio, especially when interest rates are favorable.

The history of bonds dates back centuries, with governments and corporations using them to finance projects and manage debt. In the modern era, the bond market has become increasingly complex, with a wide variety of bond types and sophisticated trading strategies. Tax laws governing bond investments have also evolved over time, making it essential for investors to stay informed about current regulations. Understanding the historical context and debunking common myths can help investors make more informed decisions about their bond portfolios and their tax planning strategies.

Unveiling the Hidden Secrets of Bond Investment Tax Planning

One hidden secret is the power of tax-loss harvesting. This involves selling bonds that have decreased in value to realize a capital loss, which can then be used to offset capital gains from other investments. While seemingly counterintuitive, this strategy can significantly reduce your overall tax liability. Another secret lies in understanding the concept of "original issue discount" (OID) bonds. OID bonds are issued at a discount to their face value, and the difference is treated as taxable interest income over the life of the bond. Proper accounting for OID is crucial to avoid unexpected tax surprises.

Furthermore, the location of your bond investments can have a significant impact on your tax bill. Holding taxable bonds in tax-advantaged accounts like 401(k)s or IRAs can shield the interest income from current taxation, allowing your investments to grow tax-deferred or even tax-free, depending on the account type. Conversely, holding tax-exempt municipal bonds in a tax-advantaged account provides no additional benefit and may even be counterproductive. These are just a few of the hidden secrets that can unlock significant tax savings in bond investing.

Recommendations for Tax-Efficient Bond Investing

My top recommendation is to consult with a qualified financial advisor and tax professional. They can assess your individual circumstances, risk tolerance, and tax situation to develop a personalized bond investment strategy. Don't be afraid to ask questions and seek clarification on any aspects of bond taxation that you find confusing. Second, consider diversifying your bond portfolio across different types of bonds (Treasuries, corporates, munis) and maturities to manage risk and optimize returns. Third, regularly review your portfolio to ensure it aligns with your investment goals and tax planning strategies. Tax laws can change, so it's important to stay informed and make adjustments as needed.

Finally, take advantage of available tax-advantaged accounts like 401(k)s, IRAs, and 529 plans to shelter your bond investments from taxation. By following these recommendations, you can build a tax-efficient bond portfolio that provides a stable income stream and helps you achieve your financial goals.

Bond Laddering and Tax Implications

Bond laddering is a strategy where you purchase bonds with staggered maturity dates. For example, you might buy bonds that mature in one year, two years, three years, and so on. This approach offers several advantages, including diversification of interest rate risk and a steady stream of income as bonds mature. When it comes to tax implications, bond laddering can provide more flexibility in managing your tax liabilities. As bonds mature, you can choose to reinvest the proceeds in similar bonds, potentially deferring capital gains taxes if you sell the bonds at a profit. Alternatively, if you need the cash, you can sell the maturing bonds and pay any applicable taxes.

Furthermore, bond laddering allows you to strategically allocate your investments based on your tax bracket. If you anticipate being in a lower tax bracket in the future, you can structure your ladder so that more bonds mature during that period, reducing your overall tax burden. Bond laddering is a simple yet effective strategy for managing both risk and taxes in your fixed income portfolio.

Practical Tips for Bond Investment Tax Planning

One practical tip is to keep meticulous records of all your bond transactions, including purchase dates, sale dates, and interest income received. This will make it much easier to accurately report your income and calculate your capital gains or losses when filing your taxes. Another tip is to be aware of the "wash sale" rule, which prevents you from claiming a capital loss if you repurchase the same or substantially identical bond within 30 days of selling it at a loss. This rule is designed to prevent taxpayers from artificially generating losses for tax purposes.

Finally, consider using tax-efficient investment vehicles like exchange-traded funds (ETFs) that track bond indices. Bond ETFs can offer diversification and liquidity, and they often have lower expense ratios than actively managed bond funds. By implementing these practical tips, you can streamline your bond investment tax planning and minimize your tax liabilities.

Understanding State and Local Tax Exemptions

The tax-exempt status of municipal bonds can vary significantly depending on your state of residence. Generally, if you purchase municipal bonds issued by your state, the interest income will be exempt from both federal and state income taxes. However, if you purchase municipal bonds issued by another state, the interest income may be subject to state income tax in your state of residence. Some states have reciprocal agreements that allow residents to purchase bonds from neighboring states and still receive the state tax exemption. It's essential to understand the specific rules in your state to maximize the tax benefits of municipal bonds.

Furthermore, some states have specific types of municipal bonds that offer enhanced tax benefits, such as those issued to finance certain types of projects. These "private activity bonds" may be subject to the alternative minimum tax (AMT) at the federal level, so it's important to consult with a tax professional to determine whether they are suitable for your situation.

Fun Facts About Bond Investments

Did you know that the first bond was issued in 1693 by the Bank of England to finance the war against France? Or that the largest bond market in the world is the U.S. Treasury market? Another interesting fact is that the term "bond" comes from the practice of physically binding together debt certificates with a ribbon.

Bond markets play a crucial role in the global economy, providing governments and corporations with a way to raise capital for various purposes. The yield on a bond is inversely related to its price, meaning that when interest rates rise, bond prices tend to fall, and vice versa. Understanding these fun facts can provide a deeper appreciation for the role of bonds in the financial system.

How to Choose the Right Bonds for Your Portfolio

Choosing the right bonds for your portfolio depends on several factors, including your risk tolerance, investment goals, and tax situation. If you are a conservative investor seeking safety and stability, you may want to focus on government bonds and high-quality corporate bonds. If you are looking for higher yields and are willing to take on more risk, you may consider investing in lower-rated corporate bonds or emerging market bonds. From a tax perspective, if you are in a high tax bracket, municipal bonds may be an attractive option due to their tax-exempt status.

It's also important to consider the maturity of the bonds you choose. Short-term bonds are less sensitive to interest rate changes but offer lower yields, while long-term bonds offer higher yields but are more susceptible to interest rate risk. A diversified bond portfolio that includes bonds with varying maturities can help you balance risk and return. Consulting with a financial advisor can help you determine the optimal bond allocation for your specific needs.

What If Interest Rates Rise?

Rising interest rates can have a negative impact on bond prices. When interest rates go up, the value of existing bonds with lower interest rates tends to decline. This is because investors can purchase newly issued bonds with higher yields, making older bonds less attractive. However, the impact of rising interest rates on your bond portfolio depends on the maturity of your bonds. Short-term bonds are less sensitive to interest rate changes than long-term bonds. If you expect interest rates to rise, you may want to consider shortening the duration of your bond portfolio by investing in short-term bonds or bond ETFs.

Furthermore, rising interest rates can create opportunities to reinvest in higher-yielding bonds as existing bonds mature. By reinvesting at higher rates, you can potentially increase your overall income from your bond portfolio.

A Listicle of Tax-Saving Bond Strategies

Here's a quick listicle of tax-saving bond strategies:

- Invest in municipal bonds to receive tax-exempt interest income.

- Hold taxable bonds in tax-advantaged accounts like 401(k)s or IRAs.

- Utilize tax-loss harvesting to offset capital gains with capital losses.

- Consider bond laddering to manage interest rate risk and tax liabilities.

- Be aware of the wash sale rule to avoid disallowing capital losses.

- Keep accurate records of all your bond transactions.

- Consult with a tax professional for personalized advice.

By implementing these strategies, you can significantly reduce your tax burden and enhance the after-tax performance of your bond investments.

Question and Answer

Q: What are the main types of bonds that offer tax advantages?

A: Municipal bonds are the primary type of bond that offers tax advantages. The interest income from most municipal bonds is exempt from federal income tax, and may also be exempt from state and local taxes if you reside in the state of issuance.

Q: How can I use tax-loss harvesting to reduce my tax liability?

A: Tax-loss harvesting involves selling bonds that have decreased in value to realize a capital loss. You can then use this capital loss to offset capital gains from other investments, reducing your overall tax liability.

Q: What is the "wash sale" rule and how does it affect bond investing?

A: The "wash sale" rule prevents you from claiming a capital loss if you repurchase the same or substantially identical bond within 30 days of selling it at a loss. This rule is designed to prevent taxpayers from artificially generating losses for tax purposes.

Q: Where should I hold my taxable bonds to minimize my tax bill?

A: It's generally best to hold taxable bonds in tax-advantaged accounts like 401(k)s or IRAs. This can shield the interest income from current taxation, allowing your investments to grow tax-deferred or even tax-free, depending on the account type.

Conclusion of Bond Investment Tax Planning: Fixed Income Strategies

Effectively managing the tax implications of your bond investments is essential for maximizing your after-tax returns. By understanding the different types of bonds, their unique tax treatments, and the strategies available to minimize your tax liabilities, you can build a tax-efficient fixed income portfolio that helps you achieve your financial goals. Remember to consult with a qualified financial advisor and tax professional to develop a personalized strategy that aligns with your individual circumstances.

Post a Comment